The supply shock that was already in progress

Before a single shot was fired in the conflict that effectively closed the Strait of Hormuz in early 2026, the US solar module supply chain was already under significant strain. Understanding the current situation requires understanding the pre-existing conditions that set this into motion.

The US solar market entered 2026 navigating an overlapping set of supply constraints that had been building since 2023. Anti-Dumping and Countervailing Duty determinations targeting Southeast Asian manufacturers, the tightening of Foreign Entity of Concern (FEOC) compliance requirements, and sustained tariff uncertainty had already forced a significant restructuring of module procurement patterns. Median US module pricing rose 14% between January and November 2025, reaching $0.28 per watt in Q1 2026 — elevated well above the $0.25 levels of early 2025.

India had emerged as the primary non-Chinese source of modules entering the US market, accounting for the vast majority of imports as Southeast Asian supply was redirected and Chinese modules faced prohibitive tariff exposure. But India's rise as a module exporter came with its own structural vulnerability: a significant gap between module assembly capacity (estimated above 100 GW) and domestic solar cell manufacturing capacity, which remains considerably lower. India's own ALMM List-II requirements, mandating domestically manufactured cells for certain project categories from mid-2026, were already expected to create temporary supply tightness.

The safe harbor cycle added a further structural layer. The OBBBA, signed July 4, 2025, triggered two simultaneous demand surges — a residential installation rush before the December 2025 ITC expiry, and an unprecedented utility-scale procurement wave as developers safe-harbored between 216 and 240 GWdc of capacity ahead of the July 2026 deadline. Manufacturers ramped up to meet both. When procurement concluded and policy uncertainty suppressed new development, order volumes dropped sharply. Demand has since recovered on the back of data center and industrial re-shoring growth — but manufacturers cannot ramp instantly. That gap between recovering demand and available production capacity is a structural contributor to today's extended lead times.

These were the conditions before the closure of the Hormuz Strait.

What the Strait of Hormuz closure means for solar supply chains

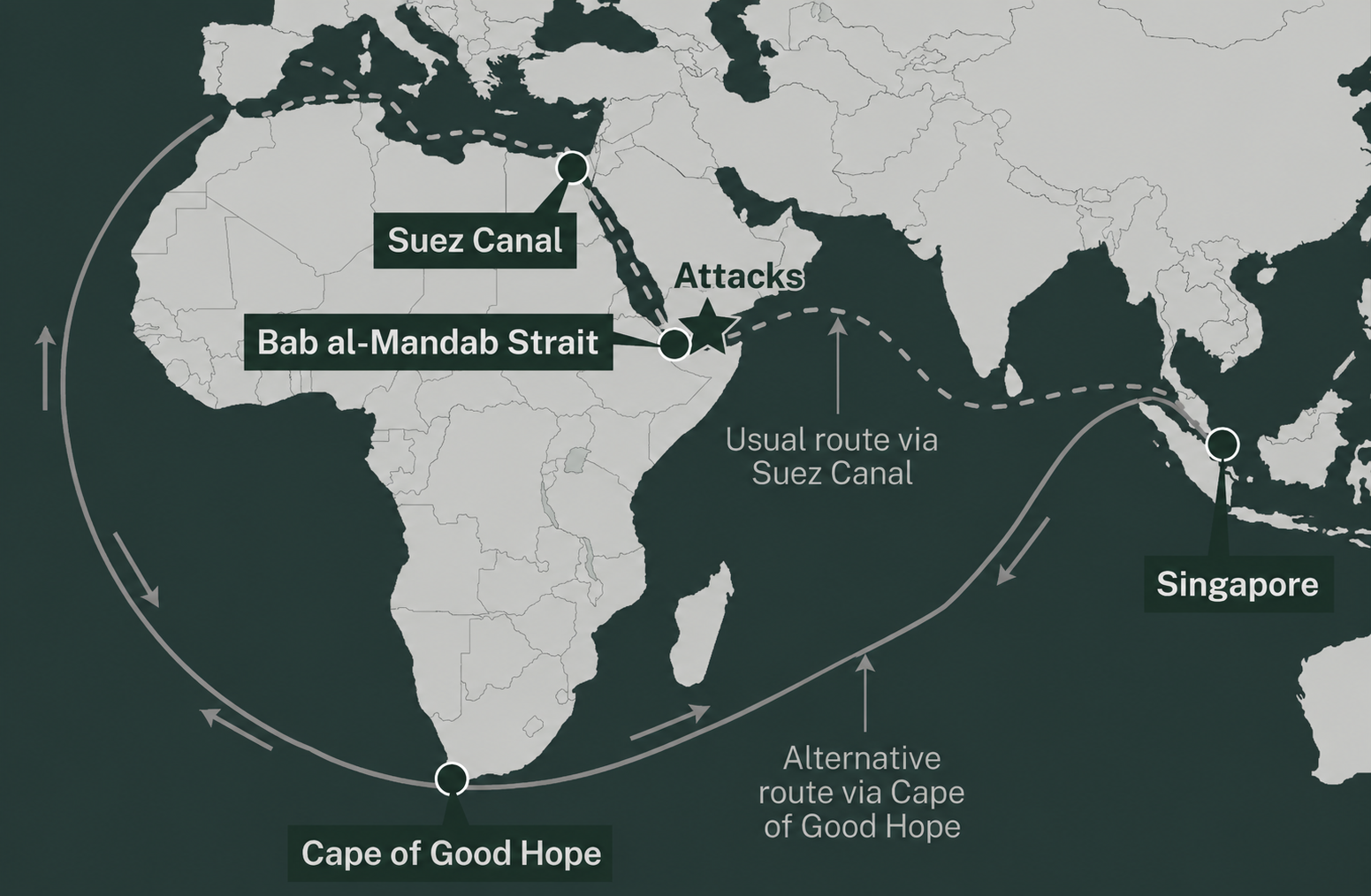

The Strait of Hormuz is not a solar supply route. Solar modules travel primarily from Asia to the US via Pacific shipping lanes, not through the Persian Gulf. The impact is made indirectly, through four factors that combine to increase price pressure.

First, fuel cost escalation. The Strait carries approximately 20% of global seaborne oil trade and significant volumes of LNG. With ship transits collapsing from 130 per day to 6 in March 2026, Brent crude rose above $90 per barrel immediately and has been oscillating between $85 and $115 per barrel until early June. Bunker fuel — the marine diesel that powers container shipping — is directly priced off crude. Higher bunker fuel costs flow through to every freight rate globally, not just routes through the Persian Gulf. Shipping costs for Asia-to-US container cargo on Pacific routes are elevated as a consequence.

Second, vessel and capacity displacement. The Cape of Good Hope rerouting — the primary alternative for cargo that previously transited the Strait or the Red Sea — adds 3,500 to 4,000 nautical miles and 10 to 14 days to voyage times. Vessels that would previously have served short-haul Gulf routes are now tied up on extended Cape routes, tightening global vessel availability. This is the same dynamic that drove container freight rates to record levels during the COVID disruption — the global fleet has a finite capacity, and rerouting consumes it.

Third, war risk insurance premiums. Shipping insurance costs have surged across all routes since the escalation. Even vessels with no Gulf exposure are facing higher insurance costs as global maritime risk is repriced. These costs are passed through as surcharges on freight contracts.

Lastly, the disruption of Jebel Ali, the world's ninth largest container port, and the primary transshipment hub connecting South and Southeast Asian exporters to global markets. A missile strike on March 1, 2026, caused inbound container flow to collapse from over 3,800 TEU per day to near zero within two weeks. Major carriers suspended Gulf routes or applied emergency surcharges of up to $4,000 per container. Alternative hubs — Salalah, Khor Fakkan — lack the capacity to absorb equivalent volume, creating congestion and schedule uncertainty across Indian Ocean shipping lanes well beyond the Strait itself.

The net effect for solar module procurement: landing costs from Indian and Southeast Asian suppliers have increased materially, adding further pressure to prices already elevated by tariff enforcement and FEOC compliance costs.

The procurement lead time crisis

The more immediate operational problem for project developers and asset owners is not price — it is availability.

SEIA's Q4 2025 report noted module shortages and delivery delays in the final quarter of 2025, with manufacturers and distributors reported to be sold out of both domestic and imported modules through the end of 2026. US solar companies are now placing purchase orders 6 to 9 months ahead of schedule to lock in supply before the next policy shift changes the cost structure.

For projects targeting 2026 or early 2027 completion dates, this means procurement decisions that would historically have been made 2 to 3 months before delivery need to be made now. That is, if the supply has not already been locked. For projects that have not yet begun procurement, availability is a genuine risk, not just a cost management question.

High-voltage transformer lead times compound this. Since 2023, the procurement departments have accepted long lead times. But recent reports indicate that lead times have increased to up to 12 months for MW transformers and are stretching 2 to 4 years for HV transformers. A project that identifies a module procurement window but has not already secured transformer supply is not actually in a position to execute.

The transformer bottleneck is particularly difficult to resolve through standard procurement because the manufacturers with available capacity are largely invisible to international buyers. Tier 2 transformer suppliers in the EU and Asia — many of whom hold the technical capability to meet utility-scale specifications — operate primarily as domestic-market businesses without international sales infrastructure. They are not listed on procurement platforms, do not respond to cold RFQs, and are not accessible without existing relationships. If a solar company has existing Tier-2 partnerships, the HV transformers lead time can effectively be reduced to 6 months for qualifying projects, but in most cases, the 2-4 year market average is the realistic planning assumption.

Impact on Repowering

For asset owners managing existing solar portfolios, the supply chain disruption creates a specific and underappreciated risk.

Repowering projects for assets in the 8–15 year age window are already operationally compelling. But repowering requires modules. And the module market that a repowering project enters in late 2026 or 2027 is not the market that existed when most repowering financial models were built.

Standard modules — already problematic for legacy racking compatibility reasons — are in constrained supply with extended lead times and elevated prices. For facilities where module dimensions are not flexible (i.e., where standard current-generation panels do not fit the existing racking without modification), the lead time for compatible supply is even more uncertain than for standard procurement.

Custom module manufacturing — specifying panels to match the dimensional and electrical requirements of an existing installation — has a lead time advantage in the current environment that is not immediately obvious. Custom manufacturing slots are planned and scheduled in advance. A committed manufacturing relationship protects you from competing in the spot market at the peak of a supply squeeze, allowing you to negotiate the price and delivery schedule that meets your needs.

For repowering projects, the custom manufacturing approach addresses both the compatibility and availability constraints in the current market. Because production runs against a committed order and planned manufacturing schedule, lead time from order confirmation to production completion can be as short as 60 to 90 days. The distinction matters in the current environment: a project with a committed manufacturing relationship can not only save on repowering costs by preserving existing infrastructure but also reduce procurement time by as much as 4 times compared to standard modules.

The tariff overlay

Layered onto the logistics disruption is a domestic policy environment that continues to reshape module pricing and supplier eligibility.

FEOC compliance requirements, tightened under Treasury Department rules, have eliminated certain module supply sources for projects seeking ITC eligibility. AD/CVD determinations targeting India carried preliminary CVD rates as high as 126% in February 2026, with final determinations expected in July. Indian module exports to the US dropped 30% in H1 2025 in response to earlier scrutiny. The US-India trade deal announced in 2026, reducing reciprocal tariffs to 18% from 25%, has partially offset this, but the uncertainty remains.

Wood Mackenzie's modeling suggests that under a sustained high-tariff scenario, US solar project construction costs could increase by up to 15% compared to pre-tariff baselines. Under current conditions, a US utility-scale solar project is already estimated to cost 54% more than a comparable project in Europe.

For asset owners, the practical consequence is this: the module cost assumptions built into repowering or new-build financial models before 2025 are unlikely to be accurate. Any capex analysis that has not been refreshed against current market conditions — tariffs, FEOC eligibility, freight escalation, and reduced spot availability — is working from stale numbers.

What a resilient procurement strategy looks like

The asset owners and developers best positioned in the current environment are those who make supply chain decisions early.

A resilient procurement approach in 2026 has four elements:

- Lead time as a first-order input. Module procurement timelines of 6 to 9 months, and transformer timelines of 1 to 4 years, must be incorporated into project planning from the first day of development — not flagged during engineering. A project that needs modules in Q2 2027 needs to be in procurement now.

- Supplier diversification and pre-qualification. Relying on a single sourcing geography or a narrow set of manufacturers concentrates tariff and logistics risk. Pre-qualifying multiple compliant supply sources — domestic, Indian, and other — provides flexibility when any single source faces a constraint.

- FEOC compliance management. Module supply that cannot qualify for ITC under FEOC rules effectively adds 30% to the net project cost in lost tax credit. Supplier FEOC eligibility assessment needs to be part of the module procurement qualification, not an afterthought during tax credit filing.

- Integrated supply for repowering. For repowering projects specifically, the combination of legacy racking compatibility requirements and current spot market constraints makes the case for a manufacturing relationship significantly stronger than it was two years ago. The ability to specify and pre-plan a custom module order, with a committed delivery schedule, is a meaningful operational and financial advantage in the current environment.

The structural picture

The Hormuz disruption is an acute event layered on top of structural conditions that were already reshaping solar supply chains. The conflict will eventually resolve, shipping routes will normalize, and fuel costs will partially retreat. But the FEOC rules, tariff uncertainty, interconnection constraints, and manufacturing capacity gaps will continue to shape the picture.

The solar industry is in a period of genuine supply chain transition — from a world where Chinese-manufactured modules at commodity prices were the default, to a world where domestic manufacturing, diversified sourcing, and compliance-driven procurement are the operating reality. That transition is incomplete, and the Hormuz disruption has accelerated its friction. Adding to this, the Chinese government has effectively stopped fierce price competition among domestic manufacturers, deliberately reducing the supply elasticity that once made the global module market relatively forgiving of procurement delays.

Asset owners who treat supply chain resilience as a procurement function — buying modules when needed at prevailing market conditions — are systematically exposed to this transition. The data of the past 18 months has made supply chain risks unambiguous. The question is whether they are being managed proactively.

.svg)